Why Adding Your Property Manager as "Additional Insured" is a Must-Do

Why Adding Your Property Manager as "Additional Insured" is a Must-Do

US existing-home sales declined 2.4% month-over-month as of the last measure, according to the National Association of REALTORS® (NAR), reversing February’s sales gain of 14.5%. Fluctuations in mortgage interest rates have caused buyers to pull back, with pending sales dropping 5.2% month-over-month. Meanwhile, the median existing-home sales price declined for the second month in a row, falling 0.9% nationally from the same time last year, the largest year-over-year decline since January 2012, according to NAR.

New listings decreased by 21.1% for residential homes and 33.2% for townhouse/condo homes. Pending sales decreased by 18% for residential homes and 22% for townhouse/condo homes. Inventory decreased by 1.7% for residential homes and 10.8% for townhouse/condo homes.

Median sales price increased 5.3% to $276,000 for residential homes and 3.3% to $219,000 for townhouse/condo homes. Days on market increased 12% for residential homes and 48% for townhouse/condo homes. Months supply of inventory increased by 27.3% for residential homes and 9.1% for townhouse/condo homes.

https://www.stlrealtors.com/pages/housingreport/

St. Louis is a bustling city with a rich history and a diverse economy. If you're a property owner in St. Louis, you know that managing your properties can be a challenge, whether you're dealing with tenant issues or maintenance problems. That's where St. Louis property management comes in.

What is St. Louis Property Management? St. Louis property management is a service that helps property owners manage their rental properties. It includes a wide range of services, such as tenant screening, rent collection, property maintenance, and legal compliance. Property management companies in St. Louis specialize in managing single-family homes, multi-family properties, apartments, and commercial buildings.

Why Choose a St. Louis Property Management Company? There are many benefits to choosing a St. Louis property management company to manage your properties. Here are a few reasons why:

Save Time and Energy: Property management can be time-consuming and stressful, especially if you have multiple properties. A property management company can handle all of the day-to-day tasks, so you don't have to.

Tenant Screening: Finding reliable tenants is key to running a successful rental property. A property management company can handle tenant screening, including credit checks, background checks, and reference checks, to help ensure that you find the right tenants for your properties.

Rent Collection: Collecting rent can be a hassle, especially if you have tenants who are late on payments. A property management company can handle rent collection for you, and can even evict non-paying tenants if necessary.

Maintenance and Repairs: Property maintenance can be costly and time-consuming. A property management company can handle maintenance and repairs for you, which can save you money and reduce your stress levels.

Legal Compliance: Property management companies are well-versed in local, state, and federal laws and regulations. They can ensure that you're in compliance with all relevant laws, which can help protect you from legal issues.

Choosing the Right St. Louis Property Management Company If you're considering hiring a St. Louis property management company, it's important to choose the right one. Here are a few things to look for:

Experience: Look for a property management company with experience managing properties similar to yours.

Reputation: Check online reviews and talk to other property owners to gauge a company's reputation.

Services and Guarantees: Make sure the property management company offers the services and Guarantees you need.

Fees: Understand the fees associated with property management, and make sure they fit your budget.

In conclusion, if you're a property owner in St. Louis, a property management company can help make your life easier. By handling everything from tenant screening to maintenance and repairs, property management companies can save you time, money, and stress. Just be sure to choose the right St. Louis property management company for your needs.

For more information on property management by Avenue please visit LeasingSTL.com

“Many downsizers expect to improve their retirement income stream if their new home costs less than what their old house sells for. Lower utility costs, insurance and property taxes — as well as investment returns on the proceeds — can also improve the bottom line.”

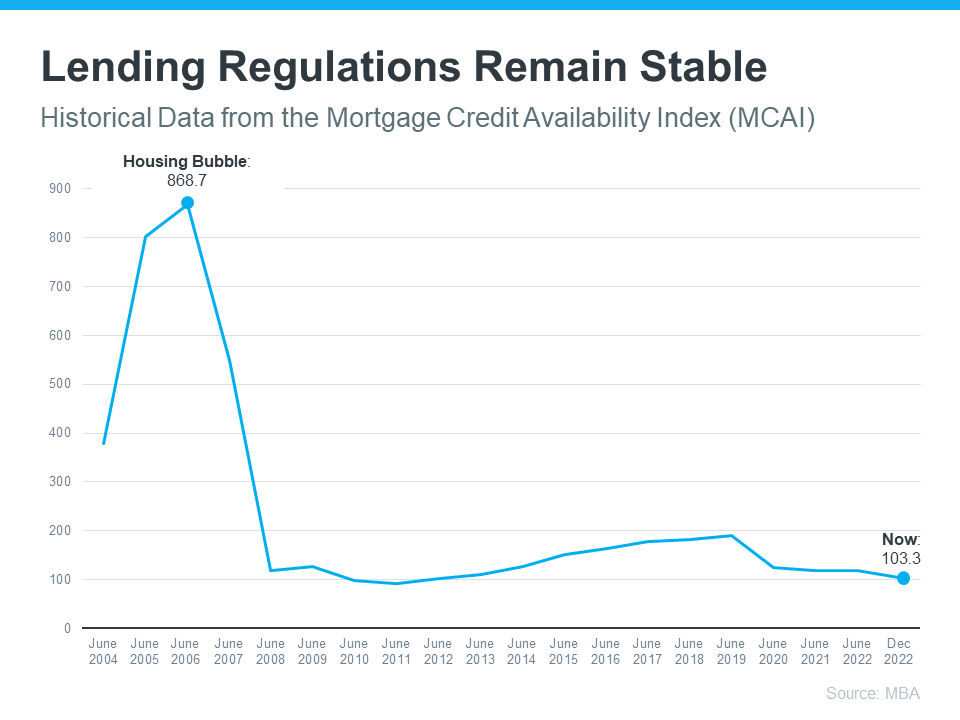

67% of Americans say a housing market crash is imminent in the next three years. With all the talk in the media lately about shifts in the housing market, it makes sense why so many people feel this way. But there’s good news. Current data shows today’s market is nothing like it was before the housing crash in 2008.

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance an existing one.

As a result, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

The graph below uses data from the Mortgage Bankers Association (MBA) to help tell this story. In this index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards have helped prevent a situation that could lead to a wave of foreclosures like the last time.

Another difference is the number of homeowners that were facing foreclosure when the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM to show the difference between last time and now:

So even as foreclosures tick up, the total number is still very low. And on top of that, most experts don’t expect foreclosures to go up drastically like they did following the crash in 2008. Bill McBride, Founder of Calculated Risk, explains the impact a large increase in foreclosures had on home prices back then – and how that’s unlikely this time.

“The bottom line is there will be an increase in foreclosures over the next year (from record level lows), but there will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.”

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just 2.7-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

If recent headlines have you worried we’re headed for another housing crash, the data above should help ease those fears. Expert insights and the most current data clearly show that today’s market is nothing like it was last time.

What does the rest of the year hold for the housing market? Here’s what experts have to say about what lies ahead.

Home prices are projected to rise and so are mortgage rates. Experts are also forecasting another strong year for home sales as people move to meet their changing needs.

Let’s connect so you can make your best move this year.

With a limited number of homes for sale today and so many buyers looking to make a purchase before mortgage rates rise further, bidding wars are common. According to the latest report from the National Association of Realtors (NAR), nationwide, homes are getting an average of 4.8 offers per sale. Here’s a look at how that breaks down state-by-state (see map below):

The same report from NAR shows the average buyer made two offers before getting their third offer accepted. In this type of competitive housing market, it’s important to know what levers you can pull to help you beat the competition. While a real estate professional is your ultimate guide to presenting a strong offer, here are a few things you could consider.

When you think of sweetening the deal for sellers, the first thought you likely have is around the price of the home. In today’s housing market, it’s true more homes are selling for over asking price because there are more buyers than there are homes for sale. You just want to make sure your offer is still within your budget and realistic for the market value in your area – that’s where a local real estate professional can help you through the process. Bankrate says:

“Simply put, being willing to pay more money than other buyers is one of the best ways to get your offer accepted. You may not have to increase it by a lot — it’ll depend on the area and other factors — so look to your real estate agent for guidance.”

You could also consider putting down a larger deposit up front. An earnest money deposit is a check you write to go along with your offer. If your offer is accepted, this deposit is credited toward your home purchase. NerdWallet explains how it works:

“A typical earnest money deposit is 1% to 2% of the home’s purchase price, but the amount varies by location. A higher earnest money deposit may catch a seller’s attention in a hot housing market.”

That’s because it shows the seller you’re seriously interested in their house and have already set aside money that you’re ready to put toward the purchase. Talk to a professional to see if this is something you can do in your area.

Another option is increasing how much of a down payment you’re going to make. The benefit of a higher down payment is you won’t have to finance as much. This helps the seller feel like there’s less risk of the deal or the financing falling through. And if other buyers put less down, it could be what helps your offer stand out from the crowd.

Realtor.com points out that while increasing these financial portions of the deal can help, they’re not your only options:

“. . . Price is not the only factor sellers weigh when they look at offers. The buyer’s terms and contingencies are also taken into account, as well as pre-approval letters, appraisal requirements, and the closing time the buyer is asking for.”

When it’s time to make an offer, partner with a trusted professional. They have insight into what sellers are looking for in your local market and can give you expert advice on what levers you may or may not want to pull when it’s time to write an offer.

From a non-financial perspective, this can include things like flexible move-in dates or minimal contingencies (conditions you set that the seller must meet for the purchase to be finalized). For example, you could make an offer that’s not contingent on the sale of your current home. Just remember, there are certain contingencies you don’t want to forego, like your home inspection. Ultimately, the options you have can vary state-to-state, so it’s best to lean on an expert real estate professional for guidance.

In today’s hot housing market, you need a partner who can serve as your guide, especially when it comes to making a strong offer. Let’s connect so you have a trusted resource and coach on how to make the strongest offer possible for your specific situation.

In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.

With today’s real estate market moving as fast as it is, working with a real estate professional is more essential than ever. They have the skills, experience, and expertise it takes to navigate the highly detailed and involved process of selling a home. That may be why the percentage of people who list their houses on their own, known as a FSBO or For Sale By Owner, has reached its lowest point since 1985 (see graph below):

Before you decide which projects and repairs to take on, connect with a real estate professional. They have first-hand experience with today’s buyers, what they expect, and what you need to do to make sure your house shows well.

If you don’t lean on their expertise, you may spend your time and money on something that isn’t essential. That’s because, in today’s low-inventory market, buyers are willing to take on more of the renovation work themselves. A survey from Freddie Mac finds that:

“. . . nearly two-in-five potential homebuyers would consider purchasing a home requiring renovations.”

A professional can help you decide what you need to tackle. It’s not canned advice you could find online – it’s recommendations specific to your house and your area.

Today, the average home is getting 4.8 offers per sale according to recent data from the National Association of Realtors (NAR), and that competition is pushing prices up. While that’s promising for you as a seller, it’s important to understand your agent’s role in bringing buyers in.

Real estate professionals have an assortment of tools at their disposal, such as social media followers, agency resources, and the MLS to ensure your house is viewed by the most buyers. According to realtor.com:

“Only licensed real estate agents can list homes on the MLS, which is a one-stop online shop of sorts for getting a house seen by thousands of agents and home buyers. . . . This is certainly one of many good reasons why the majority of home sellers decide to employ the services of a listing agent rather than going it alone.”

Without access to these tools, your buyer pool is limited. And you want more buyers to view your house since buyer competition can drive your final sales price higher.

Today, more disclosures and regulations are mandatory when selling a house. That means the number of legal documents you’ll need to juggle is growing. That’s why Investopedia says:

“One of the biggest risks of FSBO is not having the experience or expertise to navigate all of the legal and regulatory requirements that come with selling a home.”

A real estate professional knows exactly what needs to happen, what all the paperwork means, and how to work through it efficiently. They’ll help you review the documents and avoid any costly missteps that could occur if you try to handle them on your own.

If you sell without a professional, you’ll also be solely responsible for all the negotiations. That means you’ll have to coordinate with:

The buyer, who wants the best deal possible

The buyer’s agent, who will use their expertise to advocate for the buyer

The inspection company, which works for the buyer and will almost always find concerns with the house

The appraiser, who assesses the property’s value to protect the lender

Instead of going toe-to-toe with all these parties alone, lean on an expert. They’ll know what levers to pull, how to address everyone’s concerns, and when you may want to get a second opinion.

If you sell your house on your own, you may over or undershoot your asking price. That could mean you’ll leave money on the table because you priced it too low or your house will sit on the market because you priced it too high. Pricing a house requires expertise. Investopedia explains it like this:

“. . . There is no easy or universal way to determine market value for real estate.”

Real estate professionals know the ins and outs of how to price your house accurately and competitively. To do so, they compare your house to recently sold homes in your area and factor in the current condition of your house. These factors are key to making sure it’s priced to move quickly while still getting you the highest possible final sale price.

There’s a lot that goes into selling your house. Instead of tackling it alone, let’s connect so you have an expert on your side throughout the entire process.

When it comes to buying a home, it can feel a bit intimidating to know how much you need to save and where to find that information. But you should know, you’re not expected to have all the answers yourself. There are many trusted professionals who can help you understand your finances and what you’ll need to budget for throughout the process.

To get you started, here are a few things experts say you should plan for along the way.

As you set your savings goal for your purchase, your down payment is likely already top of mind. And, like many other people, you may believe you need to set aside 20% of the home’s purchase price for that down payment – but that’s not always the case. The National Association of Realtors (NAR) says:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership. Having this knowledge is critical to know what to save . . .”

The good news is, you may be able to put as little as 3.5% (or even 0%) down in some situations. To understand your options, partner with a trusted professional who can go over the various loan types, down payment assistance programs, and what each one requires.

Another item you may want to plan for is an earnest money deposit. While it isn’t required, it’s common in today’s highly competitive market because it can help your offer stand out in a bidding war.

So, what is it? It’s money you pay as a show of good faith when you make an offer on a house. This deposit works like a credit. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. It’s not an added expense, it’s just paying some of that up front. First American explains what it is and how it works:

“The deposit made from the buyer to the seller when submitting an offer. This deposit is typically held in trust by a third party and is intended to show the seller you are serious about purchasing their home. Upon closing the money will generally be applied to your down payment or closing costs.”

In other words, an earnest money deposit could be the very first check you’ll write toward your purchase. The amount varies by state and situation. Realtor.com elaborates:

“The amount you’ll deposit as earnest money will depend on factors such as policies and limitations in your state, the current market, what your real estate agent recommends, and what the seller requires. On average, however, you can expect to hand over 1% to 2% of the total home purchase price.”

Work with a real estate advisor to understand any requirements in your local area and what they’ve recommended for other buyers in your market. They’ll help you determine if it’s something that could be a useful option for you.

The next thing to plan for is your closing costs. The Federal Trade Commission (FTC) defines closing costs as:

“The upfront fees charged in connection with a mortgage loan transaction. …generally including, but not limited to a loan origination fee, title examination and insurance, survey, attorney’s fee, and prepaid items, such as escrow deposits for taxes and insurance.”

Basically, your closing costs cover the fees for various people and services involved in your transaction. NAR has this to say about how much to budget for:

“A home costs more than just the sale price. For example, closing costs—which make up about 2% to 5% of the home’s purchase price—are a major added expense…Lenders provide a Closing Disclosure at least three business days prior to closing on a mortgage. But buyers will need to budget for these added costs ahead of time to avoid sticker shock days before closing.”

The key takeaway is savvy buyers plan ahead for these expenses so they can come into the process prepared. Freddie Mac sums it up like this:

“If you’re in the market to buy a home, your down payment is probably top of mind. And rightly so – it’s likely the biggest cost of homebuying. However, it is not the only cost and it’s critical you understand all your expenses before diving in. The more prepared you are for your down payment, closing and other costs, the smoother your homebuying journey will be.”

Knowing what to budget for in the homebuying process is essential. To make sure you understand these and any other expenses that may come up, let’s connect so you have reliable expertise on what to expect when you buy a home.

Are you thinking about selling your house? If so, you may want to make it a priority to start the process soon. According to realtor.com, the sweet spot for sellers is just around the corner. In a recent study, experts analyzed housing market trends by looking at data from the past several years (excluding 2020, since it was an atypical year). When applied to the current market, experts determined the ideal week to list a house this year. The research says:

“Home sellers on the fence waiting for that perfect moment to sell should start preparations, because the best time to list a home in 2022 is approaching quickly. The week of April 10-16 is expected to have the ideal balance of housing market conditions that favor home sellers, more so than any other week in the year.”

If you’ve been putting your move on the back burner waiting for the ideal time to sell, you should know your golden window of opportunity is coming up. If you’re able to get your house ready quickly, here’s what you can expect from that week.

The article expects higher buyer demand based on what’s happened in previous years. This could result in increased competition among buyers and ultimately a bidding war over your house. And since mortgage rates recently ticked up over 4%, chances are good that analysis is right. When rates rise, experts say buyers often hurry to make their purchase before rates climb higher. As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“. . . Buyers are rushing to lock in lower rates as the outlook is for even higher mortgage rates in the following months.”

Additionally, the realtor.com analysis shows houses sell even faster during this week of the year, likely due to the heightened buyer demand. If you work with a trusted real estate professional to price your house right, it should sell quickly. And when homes are already selling in just 18 days according to NAR, that could set you up for a big win.

Since the beginning of the year, the number of homes available for sale has been at or near record lows. According to the realtor.com study, the typical trend for this week of the year is that there will be even fewer sellers on the market. If you list when inventory is low, your house will be the center of attention for eager buyers craving options.

If you’re ready to move fast, you may want to shoot for April 10th-16th as your target goal. Just remember, even if you’re not ready to list within the next couple of weeks, rest assured this is still a hot sellers’ market. If you list later in April, you’ll still be in the driver’s seat.

Ready to get the ball rolling? Let’s connect and schedule a time to go over your next steps. In the meantime, make a checklist of things you need to tackle to get your house ready. When we talk, we can prioritize your to-do list and get you on the road to selling your house.

If you’re a current homeowner, you should know your net worth just got a big boost. It comes in the form of rising home equity. Equity is the current value of your home minus what you owe on the loan. Today, you’re building that equity far faster than you may expect – and this gain is great news for you.

Here’s how it happened. Home values are on the rise thanks to low housing supply and high buyer demand. Basically, there aren’t enough homes available to meet this high buyer interest, so bidding wars are driving home prices up. When you own a home, the rising prices mean your home is worth more in today’s market. And as home values climb, your equity does too. As Dr. Frank Nothaft, Chief Economist at CoreLogic, explains:

“Home prices rose 18% during 2021 in the CoreLogic Home Price Index, the largest annual gain recorded in its 45-year history, generating a big increase in home equity wealth.”

The latest Homeowner Equity Insights from CoreLogic shed light on just how much rising home values have boosted homeowner equity. According to that report, the average homeowner’s equity has grown by $55,300 over the last 12 months.

Want to know what’s happening in your area? Here’s a breakdown of the average year-over-year equity growth for each state based on that data.

In addition to building your overall net worth, equity can also help you achieve other goals like buying your next home. It works like this: when you sell your house, the equity you built up comes back to you in the sale.

In a market where you’re gaining so much equity, it may be just what you need to cover a large portion – if not all – of the down payment on your next home. So, if you’ve been holding off on selling and worried about being priced out of your next home because of today’s home price appreciation, rest assured your equity can help fuel your move.

Equity can be a real game-changer if you’re planning to make a move. To find out just how much equity you have in your home and how you can use it to fuel your next purchase, let’s connect so you can get a professional equity assessment report on your house.

When you make a move, you want to sell your house for the highest price possible. That might be why many homeowners are eager to list in today’s sellers’ market. After all, with record-low inventory and high buyer demand, many homes are selling for more than asking price. Data from the National Association of Realtors (NAR) shows 46% of homes are selling above list price today.

But even in a market like we have now, working with an agent to set the right asking price is critical, as pricing it too high or too low could have a negative impact on your final sale. Here’s why.

The price you set for your house sends a message to potential buyers. Price it too low and you might raise questions about your home’s condition or lead buyers to assume something is wrong with the property. Not to mention, you could leave money on the table, which decreases your future buying power if you undervalue your house.

On the other hand, price it too high and you run the risk of deterring buyers. When that happens, you may have to do a price drop to try to re-ignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder why the price was reduced and what that means about the home.

In other words, think of pricing your home as a target. Your goal is to aim directly for the center – not too high, not too low, but right at market value. Pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. That makes it more likely you’ll see a bidding war, too. And when a bidding war happens, you’ll likely get an even higher final sale price. Plus, when homes are priced right, they tend to sell quickly.

To get a look into the potential downsides of over or underpricing your house and the perks that come with pricing it at market value, see the chart below:

There are several factors that go into pricing your house and balancing them is the key. That’s why it’s important to lean on an expert real estate advisor when you’re ready to move. A local real estate advisor is knowledgeable about:

The value of homes in your neighborhood

The current demand for houses in today’s market

The condition of your house and how it affects the value

A real estate professional will balance these factors to make sure the price of your house makes the best first impression and gives you the greatest return on your investment in the end.

Even in a sellers’ market, pricing your house right is critical. Don’t rely on guesswork. Let’s connect to make sure your house is perfectly priced.

Having an experienced guide coaching you through the process of buying or selling a home is important in a normal market – but today’s market is far from normal. As a result, an expert real estate advisor isn’t just good to have by your side, they’re essential.

Today’s housing market is full of extremes. Experts project mortgage rates will continue to rise this year, and that’s driving significant demand for homes as buyers want to make their purchases before rates climb even higher. At the same time, an absence of sellers is leading to record-low housing inventory. This imbalance in supply and demand is creating bidding wars and driving home price appreciation as well as considerable gains in home equity.

These market conditions can feel overwhelming, but you don’t have to go at it alone. Having a trusted expert to coach you through the process of buying or selling a home gives you clarity and confidence through each step.

Contracts – Agents help with the disclosures and contracts necessary in today’s heavily regulated environment.

Experience – In an unprecedented market, experience is crucial. Real estate professionals know the entire sales process, including how it’s changed over the past two years.

Negotiations – Your real estate advisor acts as a buffer in negotiations with all parties throughout the entire transaction and advocates for your best interests.

Education – Knowledge is power in today’s market, and your advisor will simply and effectively explain market conditions and translate what they mean for you.

Pricing – Finally, a real estate professional understands today’s real estate values when setting the price of your home or helping you make an offer to purchase one.

A real estate agent is a crucial guide through this unprecedented market, but not all agents are created equal. A true expert can carefully walk you through the whole real estate process, look out for your unique needs, and advise you on the best ways to achieve success. Finding an expert real estate advisor – not just any agent – should be your top priority when you’re ready to buy or sell a home.

It starts with trust. You’ll want to know you can trust the advice they’re giving you, so you need to make sure you’re connected with a true professional. No one can provide perfect advice because it’s impossible to know exactly what’s going to happen at every turn – especially in today’s unique market. But a true professional can give you the best possible advice based on the information and situation at hand. They’ll help you make the necessary adjustments along the way, advocate for you throughout the process, and coach you on the essential knowledge you need to make confident decisions. That’s exactly what you want and deserve.

It’s critical to have an expert on your side who’s well versed in navigating today’s rapidly changing market. If you’re planning to buy or sell a home this year, let’s connect so you have a real estate professional on your side to give you the best advice and guide you along the way.

In an annual Gallup poll, Americans chose real estate as the best long-term investment. And it’s not the first time it’s topped the list, either. Real estate has been on a winning streak for the past eight years, consistently gaining traction as the best long-term investment (see graph below):

If you’re thinking about purchasing a home this year, this poll should reassure you. Even when inflation is rising like it is today, Americans agree an investment like real estate truly shines.

With inflation reaching its highest level in 40 years, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board. That includes goods, services, housing costs, and more. But when you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increasing housing payments. James Royal, Senior Wealth Management Reporter at Bankrate, explains it like this:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

If you’re a renter, you don’t have that same benefit, and you aren’t protected from increases in your housing costs, especially rising rents.

As a homeowner, your house is an asset that typically increases in value over time, even during inflation. That‘s because, as prices rise, the value of your home does, too. And that makes buying a home a great hedge during periods of high inflation. Natalie Campisi, Advisor Staff for Forbes, notes:

“Tangible assets like real estate get more valuable over time, which makes buying a home a good way to spend your money during inflationary times.”

Housing truly is a strong investment, especially when inflation is high. When you lock in a mortgage payment, you’re shielded from housing cost increases, and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

If you’re thinking about selling your house in 2022, you truly have a once-in-a-lifetime opportunity at your fingertips. When selling anything, you always hope for strong demand for the item coupled with a limited supply. That maximizes your leverage when you’re negotiating the sale. Home sellers are in that exact situation right now. Here’s why.

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), 6.18 million homes were sold in 2021. This was the largest number of home sales in 15 years. Lawrence Yun, Chief Economist for NAR, explains:

“Sales for the entire year finished strong, reaching the highest annual level since 2006. . . . With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases.”

Demand isn’t expected to weaken this year, either. In addition, the Mortgage Finance Forecast, published last week by the Mortgage Bankers’ Association (MBA), calls for existing-home sales to reach 6.4 million homes this year.

The same sales report from NAR also reveals the months’ supply of inventory just hit the lowest number of the century. It notes:

“Total housing inventory at the end of December amounted to 910,000 units, down 18% from November and down 14.2% from one year ago (1.06 million). Unsold inventory sits at a 1.8-month supply at the present sales pace, down from 2.1 months in November and from 1.9 months in December 2020.”

The reality is, inventory decreases every year in December. That’s just how the typical seasonal trend goes in real estate. However, the following graph emphasizes how this December was lower than any other December going all the way back to 1999.

As mentioned above, when there’s strong demand for an item and a limited supply of it available, the seller has maximum leverage in the negotiation. In the case of homeowners who are thinking about selling, there may never be a better time than right now. While demand is this high and inventory is this low, you’ll have leverage in all aspects of the sale of your house.

Today’s buyers know they need to be flexible negotiators that make very competitive offers, so here are a few areas that could tip in your favor when your house goes on the market:

Competitive sales price

Flexible closing date

Potential for a leaseback to allow you more time to find a home

Minimal offer contingencies

If you’re thinking of selling your house this year, now is the optimal time to list it. Let’s connect to discuss how you can put your house on the market today.

Last week, the average 30-year fixed mortgage rate from Freddie Mac jumped from 3.22% to 3.45%. That’s the highest point it’s been in almost two years. If you’re thinking about buying a home, this news may have come as a bit of a shock. But the truth is, it wasn’t entirely unexpected. Experts have been calling for rates to rise in their 2022 projections, and the forecast is now becoming a reality. Here’s a look at the projections from Freddie Mac for this year:

Q1 2022: 3.4%

Q2 2022: 3.5%

Q3 2022: 3.6%

Q4 2022: 3.7%

As the numbers show, this jump in rates is in line with the expectations from Freddie Mac. And what they also indicate is that mortgage rates are projected to continue climbing throughout the year. But should you be worried about rising mortgage rates? What does that really mean for you?

As rates increase even modestly, they impact your monthly mortgage payment and overall affordability. If you’re looking to buy a home, rising mortgage rates should be an incentive to act sooner rather than later.

The good news is, even though rates are climbing, they’re still worth taking advantage of. Historical data shows that today’s rate, even at 3.45%, is still well below the average for each of the last five decades (see chart below):

That means you still have a great opportunity to buy now with a rate that’s better than what your loved ones may have paid in decades past. If you buy a home while rates are in the mid-3s, your monthly mortgage payment will be locked in at that rate for the life of your loan. As you can see from the chart above, a lot can change in that time frame. Buying now is a great way to protect yourself from rising costs and future rate increases while also securing your payment amount for the long term.

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“Mortgage rates surged in the second week of the new year. The 30-year fixed mortgage rate rose to 3.45% from 3.22% the previous week. If inflation continues to grow at the current pace, rates will move up even faster in the following months.”

Mortgage rates are increasing, and they’re forecast to be even higher by the end of 2022. If you’re planning to buy this year, acting soon may be your most affordable option. Let’s connect to start the homebuying process today.

If you’re following along with the news today, you’re probably hearing a lot about record-breaking home prices, rising consumer costs, supply chain constraints, and more. And if you’re thinking about purchasing a home this year, all of these inflationary concerns are likely making you wonder if you should wait to buy. Investopedia explains that during a period of high inflation, prices rise across the board. And while home prices aren’t immune from this increase, here’s why inflation shouldn’t stop you from buying a home in 2022.

Home prices have been increasing for quite some time, and experts say they’re going to continue to climb throughout 2022. So, as a buyer, how can you protect yourself from rising costs for things like food, shelter, entertainment, and other goods and services? The answer lies in housing.

Buying a home allows you to lock in your monthly mortgage payment for the foreseeable future. That means as other prices rise, your monthly payment will be consistent thanks to your fixed-rate mortgage. This gives you the peace of mind that the bulk of your housing costs is shielded from inflation.

James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

If you rent, you don’t have that same benefit and you won’t be protected from rising housing costs. As an added incentive to buy, consider that today’s mortgage interest rates are lower than they have been in decades. While inflation decreases what your dollars can buy, low mortgage rates help counteract it by boosting your purchasing power so you can get more home for your money. They also help keep your monthly payments down. This is especially important during an inflationary period because you’ll want to protect yourself from the impact of inflation as much as possible.

Ali Wolf, Chief Economist at Zonda, explains:

“If you have cash and are expecting inflation, you want to think through where you can put your money so it does not lose value. Housing is commonly looked at as a good inflation hedge, especially with interest rates so low.”

The best hedge against inflation is a fixed housing cost. That’s why you shouldn’t let it stop you from buying a home this year. Not sure where to start? Let’s connect so you have expert advice and help throughout every step of the homebuying process.

Many homeowners who plan to sell in 2022 may think the wise thing to do is to wait for the spring buying market since historically about 40 percent of home sales occur between April and July. However, this year’s expected to be much different than the norm. Here are five reasons to list your house now rather than waiting until the spring.

The ShowingTime Showing Index reports data from more than six million property showings scheduled across the country each month. In other words, it’s a gauge of how many buyers are out looking at homes at the current time.

The latest index, which covers November showings, reveals that buyers are still very active in the market. Comparing this November’s numbers to previous years, this graph shows that the index is higher than last year and much higher than the three years prior to the pandemic. Clearly, there’s an influx of buyers searching for your home.

Also, at this time of year, only those purchasers who are serious about buying a home will be in the market. You and your loved ones won’t be inconvenienced by casual searchers. Freddie Mac addresses this in a recent blog:

“The buyers who are willing to house hunt in a winter market, when there are fewer options, are typically more serious. Plus, year-end bonuses and overtime payouts give people more purchasing power.”

And that theory is proving to be true right now based on the number of buyers who have put a home under contract to purchase. The National Association of Realtors (NAR) publishes a monthly Pending Home Sales Index which measures housing contract activity. It’s based on signed real estate contracts for existing single-family homes, condos, and co-ops. The latest index shows:

“…housing demand continues to be high. . . . Homes placed on the market for sale go from ‘listed status’ to ‘under contract’ in approximately 18 days.”

Comparing the index to previous Novembers, while it’s slightly below November 2020 (when sales were pushed to later in the year because of the pandemic), it’s well above the previous three years.

The takeaway for you: There are purchasers in the market, and they’re ready and willing to buy.

The law of supply and demand tells us that if you want the best price possible and to negotiate your ideal contract terms, put your house on the market when there’s strong demand and less competition.

A recent study by realtor.com reveals that, unlike in previous years, sellers plan to list their homes this winter instead of waiting until spring or summer. The study shows that 65% of sellers who plan to sell in 2022 have either already listed their home (19%) or are planning to put it on the market this winter.

Again, if you’re looking for the best price and the ability to best negotiate the other terms of the sale of your house, listing before this competition hits the market makes sense.

In 2020, there were over 979,000 new single-family housing units authorized by building permits. Many of those homes have yet to be built because of labor shortages and supply chain bottlenecks brought on by the pandemic. They will, however, be completed in 2022. That will create additional competition when you sell your house. Beating these newly constructed homes to the market is something you should consider to ensure your house gets as much attention from interested buyers as possible.

If you’re moving into a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 5% over the next 12 months. That means it will cost you more (both in down payment and mortgage payment) if you wait. You can also lock in your 30-year housing expense with a mortgage rate in the low 3’s right now. If you’re thinking of selling in 2022, you may want to do it now instead of waiting, as mortgage rates are forecast to rise throughout the year.

Consider why you’re thinking of selling in the first place and determine whether it’s worth waiting. Is waiting more important than being closer to your loved ones now? Is waiting more important than your health? Is waiting more important than having the space you truly need?

Only you know the answers to those questions. Take time to think about your goals and priorities as we move into 2022 and consider what’s most important to act on now.

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, let’s connect so you have expert advice on the best time to put your house on the market.

Aaron Wilson

(314) 401-5012

or

Justin Hansen

(314) 246-9129

Tremendous amount of space in this incredible, newer home located on Deer Valley Ct. in beautiful St. Albans. With over 8, 650 s.f. this home has room for all your dreams. Special features include 2 main floor masters one with adjacent nursery or bonus room, a gorgeous entry with spiral staircase, formal and informal living rooms, chefs kitchen with high end appliances and a second floor bonus room. The walkout lower level stuns with a second full kitchen, game room, exercise room, custom modern gas fireplace and an additional bedroom and bath. There is also still plenty of room for storage. The entire property is brilliantly landscaped but the back yard with incredible outdoor living space is sure to impress with large, private pool with sun ledge surrounded by stone and brick patios, a fire pit and built in BBQ grill and separate pizza oven. All 3 upstairs bedrooms are private suites and there is a 3 car garage as well. There isn't much more you could want in a luxury home.

Total Rooms: 19

Hearth: 20 x 15

Hearth Level: 2 - M

Laundry Room: 10 x 8

Laundry Room Level: 2 - M

Recreation Room: 25 x 17

Recreation Room Level: 3 - U

Den Dimensions: 14 x 12

Family Room Dimensions: 17 x 17

Game/Recreation Room Dimensions: 25 x 17

Great Room Dimensions: 16 x 16

Den Level: 2 - M

Family Room Level: 1 - L

Game/Recreation Room Level: 1 - L

Great Room Level: 2 - M

Basement Description: 9 ft + pour Basement, Bathroom in Lower Level, Fireplace in Lower Level, Partially Finished Basement, Basement Rec/Family Area, Basement Sleeping Area, Basement Walk-Out

Appliances: Dishwasher, Gas Cooktop, Microwave, Range/Oven-Gas, Refrigerator, Water Softener, Wine Cooler

Bedrooms: 7

Master Bedroom Dimensions: 25 x 14

Bedroom 1 Dimensions: 21 x 13

Bedroom 2 Dimensions: 20 x 13

Bedroom 3 Dimensions: 15 x 12

Bedroom 4 Dimensions: 19 x 16

Bedroom 5 Dimensions: 17 x 13

Master Bedroom Level: 2 - M

Bedroom 1 Level: 2 - M

Bedroom 2 Level: 3 - U

Bedroom 3 Level: 2 - M

Bedroom 4 Level: 3 - U

Bedroom 5 Level: 1 - L

Total Bathrooms: 7 / 1

Full Bathrooms: 7

1/2 Bathrooms: 1

Full Bathrooms On Main Level: 3

Bathroom 1 Dimensions: 17 x 10

Bathroom 1 Level: 2 - M

Master Bathroom Description: Double Sink, Full Bath, Whirlpool & Sep Shwr

Interior Decor: Built-In Bookcases, 9' Ceilings, Open Floor Plan, 10 foot ceilings, Vaulted Ceiling, Walk-In Closets, Some Wood Floors

Window Features: Bay/Bow Window, French Door(s), Some Insulated Wndws

Kitchen: Breakfast Bar, Breakfast Room, Butler Pantry, Custom Cabinetry, Hearth Room, Solid Surface Counter, Walk-In Pantry

Breakfast Room Dimensions: 14 x 11

Breakfast Room Level: 2 - M

Dining Room Description: Separate Dining

Dining Room Dimensions: 12 x 15

Dining Room Level: 2 - M

Kitchen Dimensions: 15 x 11

Kitchen Level: 2 - M

Cooling Features: Ceiling Fan Cooling, Central-Electric Cooling, Zoned Cooling

Fireplace Features: Fireplace Type: Full Masonry Fireplace, Gas Fireplace, Fireplace Insert

Heating Features: Forced Air Heating, Zoned Heating

Private Inground Pool

Underground Util

Lot Description: Backs to Trees/Woods, Fencing, Level Lot

Lot Size Acres: 0.8300046

Lot Size Dimensions: 0.83

Lot Size Source: County Records

Lot Size Square Feet: 36155

Garage Spaces: 3

Garage Features: Garage Size: 34x21

Parking Features: Garage Door Opener, Oversize, Rear/Side Entry

Property Amenities: Private Inground Pool, Underground Util

Association: Yes

Association Fee: 1000

Association Fee Frequency: Semi-Annually

Calculated Total Monthly Association Fees: 167

Elementary School: Labadie Elem.

High School: Washington High

Middle School: Washington Middle

School District: Washington

Special Areas: Balcony, Bonus Room, Den/Office, Entry Foyer, Front/Back Stairs, Great Room, Library/Den, Main Floor Laundry

Misc Kitchen and Dining: High Spd Connection, Patio, Porch-Covered, Security Alarm-Owned, Sprinkler Sys-Inground

Annual Tax Amount: 17763

Source Listing Status: Active

County: Franklin

Tax Year: 2020

Ownership: Private

Source Property Type: Residential

Area: Washington School

Source Neighborhood: St. Albans Deer Valley

Subdivision: St. Albans Deer Valley

Lot Number: 16R

Source System Name: C2C

Coming Soon Date: 2021-08-12

Total Square Feet Living: 8684.00

Year Built: 2008

Builder Name: St. Albans Construction Co.

Construction Materials: Brick Veneer Predom

Property Age: 13

Levels or Stories: 1.5

Total Above Grade Sqft Area: 6551

Total Area Sqft: 8684

Total Below Grade Area: 2105

Architectural Style: Architecture: Other, Style: 1.5 Story

Special Utilities: Owner Occupied

Sewer: Public

Water Source: Public

*All information herein has not been verified and is not guaranteed.

Data Source: MARIS

Source's Property ID:21053187

Data Source Copyright: ©2021 Mid America Regional Information Systems Inc. All rights reserved.